The energy price forecast for 2026 does not point to meaningful near-term relief. The structural drivers pushing electricity and natural gas costs higher, such as AI-driven load growth, retiring generation capacity, tight pipeline infrastructure, and sustained LNG export demand, are not short-term phenomena. Businesses that approach 2026 with a deliberate procurement strategy, a clear understanding of their cost exposure, and a realistic view of the forward market will be in a materially better position than those that renew on autopilot or wait for conditions to improve on their own.

This article covers the key drivers behind the 2026 electricity price forecast, what the outlook means for commercial energy budgets, and the specific steps your business should take now to manage cost risk before your next contract expires.

Energy Price Forecast for 2026 at a Glance

For business decision-makers who need the headline view before diving into the detail, here is where the 2026 US energy market stands:

- Electricity Prices: Commercial electricity rates across major deregulated markets remain above historical averages. The PJM 2026/27 Base Residual Auction cleared at the FERC-imposed cap of $329.17 per MW-day, a record result that is flowing directly into commercial supply rates across the PJM footprint, affecting businesses in Pennsylvania, New Jersey, Ohio, Maryland, Illinois, and more than a dozen other states. Buyers renewing contracts in 2026 are entering a market where capacity costs alone represent a significantly higher share of their all-in supply rate than they did three to four years ago.

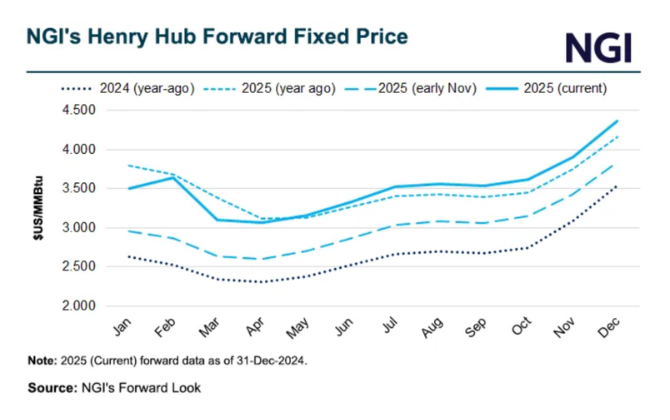

- Natural Gas Prices: Henry Hub forward prices for 2026 are directionally higher than the 2024 lows, reflecting below-average storage inventory levels entering the year and sustained LNG export demand that has raised the domestic price floor. Businesses consuming natural gas directly for heating or process use should budget for supply rates above recent historical norms. Customers in the Northeast face additional basis risk during winter peak periods when regional delivery prices can spike well above the Henry Hub benchmark.

Key Risk Drivers:

- Record PJM capacity auction results flowing through to retail electricity supply rates

- AI-driven data center load growth adding sustained demand pressure across multiple grid regions

- Natural gas storage below the five-year seasonal average, supporting higher forward prices

- Tightening reserve margins as generation retirements outpace new capacity additions

- Transmission congestion in constrained regions adding to delivered electricity costs

Business Implications:

- Budgets built on 2023 or 2024 energy cost baselines are likely understating 2026 exposure

- Fixed-rate contracts executed now lock in current market conditions and provide protection from further upside

- Index and variable rate customers retain full exposure to every risk driver listed above

- Buyers with contracts expiring in the next 60 to 180 days should be in the market now, not at expiration

Energy Price Forecast Data for 2026

The following data points reflect current forward market conditions, recent auction results, and directional market indicators across the key inputs that drive commercial electricity and natural gas costs. This section is intended as a practical planning reference for business buyers, not a comprehensive commodity market report.

Electricity

Commercial electricity prices in deregulated US markets are averaging between $0.08 and $0.14 per kWh, depending on utility territory, load profile, and contract structure, with PJM-footprint markets sitting at the higher end of that range due to capacity cost pass-throughs.

Forward electricity prices for 2026 delivery reflect sustained on-peak premiums driven by afternoon demand peaks associated with cooling load and data center consumption.

Retail supply rates for new fixed-rate contracts in PJM markets are meaningfully higher than equivalent contracts executed in 2022 or 2023, primarily due to the step-change in capacity costs following the 2025/26 and 2026/27 auction results.

Natural Gas

Henry Hub forward prices for the 2026 calendar year are trading in the $3.50 to $4.50 per MMBtu range, compared to the 2024 annual average of approximately $2.22 per MMBtu, a directional increase of 55 to 100% depending on the delivery period.

US natural gas storage inventories have trended below the five-year seasonal average for several consecutive reporting weeks, tightening the near-term supply picture and supporting forward price levels.

LNG export capacity additions have absorbed a growing share of domestic production, reducing the volume of gas available to buffer domestic demand spikes during peak periods.

Capacity

PJM’s 2026/27 Base Residual Auction cleared at $329.17 per MW-day, the FERC-imposed market cap, the highest capacity price result in the market’s history.

Capacity costs now represent an estimated 30 to 40% of the all-in commercial electricity supply rate in PJM footprint markets, up from single-digit percentages in prior auction cycles.

NYISO and ISO-NE capacity markets continue to reflect tight reserve conditions in the Northeast, with capacity prices supporting elevated all-in retail rates in New York and New England markets.

Demand

US electricity demand growth is projected to accelerate through 2026 and beyond, driven primarily by hyperscale data center buildout associated with AI infrastructure, EV charging load, and industrial electrification initiatives.

PJM has publicly projected load growth requirements that exceed historical planning assumptions by a significant margin, driven largely by data center interconnection requests in Virginia, Pennsylvania, and Ohio.

Peak demand events are occurring with greater frequency and intensity across multiple grid regions, increasing the likelihood of high-cost hours that affect both capacity tags and index rate customers.

Weather and Seasonal Risk

Winter 2025/26 storage withdrawals were above seasonal norms in several regions, leaving natural gas inventories below the five-year average heading into the 2026 injection season, a condition that historically supports elevated summer and forward winter prices.

Above-normal temperatures across the South and Midwest during summer 2025 produced several peak demand events that affected spot electricity prices and capacity tag measurement hours in PJM.

Weather-driven price volatility remains an asymmetric risk for index and variable rate customers — extreme events produce outsized cost spikes that can define the economics of an entire contract year.

Transmission

Transmission congestion costs in constrained regions, particularly in the mid-Atlantic and parts of the Midwest, are adding to the delivered cost of electricity above and beyond generation and capacity components.

Interconnection queues for new generation remain lengthy across major grid regions, meaning transmission relief from new supply is years away in most constrained markets.

Locational basis differentials between hub prices and customer delivery points continue to vary significantly, particularly for natural gas customers in the Northeast, where pipeline constraints remain a structural cost driver during winter peak periods.

What Is Driving the 2026 Energy Outlook?

Energy price forecasts are only as useful as the explanation behind them. Understanding what is actually driving costs in 2026 helps business decision-makers distinguish between temporary market noise and structural pressures that will shape energy budgets for several years to come. The three drivers below are structural. They are not resolving quickly, and they are not priced into most business energy budgets at the level they should be.

Electricity Demand Remains a Pressure Point

The US electricity system was not designed for the scale of demand growth now hitting it simultaneously from multiple directions. Artificial intelligence infrastructure alone is driving a wave of data center construction that grid operators across the country are struggling to keep pace with. In PJM, the nation’s largest wholesale electricity market, data center interconnection requests have surged to levels that have fundamentally altered the grid’s long-term load forecast. Virginia, Pennsylvania, and Ohio are among the most acutely affected states, with hundreds of gigawatts of new load requests in the interconnection queue.

Data centers are only part of the story. Electric vehicle adoption is adding baseline charging load that did not exist five years ago. Heat pump deployment is shifting natural gas heating demand onto the electric grid. Industrial electrification initiatives are adding factory-level load in regions that have seen flat or declining industrial electricity demand for decades. Each of these trends is individually significant. Together, they represent a sustained, multi-year demand growth trajectory that the existing generation and transmission infrastructure was not built to absorb without cost consequences.

For commercial energy buyers, the practical implication is straightforward: more competition for the same grid capacity means higher prices for that capacity, and those prices are already showing up in capacity auction results and forward electricity markets.

Capacity and Transmission Costs Still Matter

Capacity costs are the component of a commercial electricity bill that most business buyers understand least and that the 2026 market environment has made most consequential. In simple terms, capacity charges are what businesses pay to ensure the grid has enough generation reserved to meet peak demand, including their share of it. These costs are determined through forward auctions run by regional grid operators and then passed through to commercial customers in their retail electricity supply rates.

PJM’s 2026/27 Base Residual Auction cleared at $329.17 per MW-day, the maximum price permitted under FERC rules, a result that reflects how severely the supply-demand balance in that market has shifted. For businesses in the PJM footprint, this auction result translates directly into higher supply rates on new contracts. Capacity charges that once represented a modest fraction of the all-in electricity rate now represent an estimated 30 to 40% of what commercial customers pay for supply in affected markets.

Transmission costs are adding a second layer of pressure. As the grid carries more power over longer distances to serve load in constrained regions, congestion costs build up at specific delivery points, and those costs are ultimately borne by the customers taking delivery there. For businesses in congested areas, the gap between the regional hub price and what they actually pay at their meter has widened in ways that are not always visible until a bill review reveals the discrepancy.

The combined effect of elevated capacity costs and transmission congestion means that finding a lower supply rate is only part of the cost reduction opportunity. Understanding and managing the delivery side of the bill, through demand management, peak shaving, and capacity tag reduction strategies, is equally important in the current environment.

Natural Gas Continues to Influence Power Prices

Natural gas is the marginal fuel for electricity generation across most of the United States, meaning it is the fuel that sets the price for the last unit of electricity dispatched to meet demand at any given moment. When natural gas prices rise, wholesale electricity prices follow. This relationship is structural, and it applies in virtually every major US power market regardless of how much renewable generation is operating.

The natural gas market in 2026 is being shaped by two forces that have structurally raised the domestic price floor relative to where it sat in 2020 through 2023. First, US LNG export capacity has expanded significantly, diverting a growing share of domestic gas production to international markets where prices are higher. This has reduced the domestic supply buffer that historically kept Henry Hub prices low during periods of moderate demand. Second, natural gas storage inventories have trended below the five-year seasonal average, tightening the near-term supply picture and providing less cushion against demand spikes or production disruptions.

For a finance or operations leader trying to plan around natural gas costs in 2026, the practical translation is this: the era of sub-$3 Henry Hub gas that characterized much of the previous decade is not the planning baseline for 2026. Forward markets are pricing domestic natural gas meaningfully higher, and customers in the Northeast face additional basis risk, the spread between the Henry Hub benchmark and actual regional delivery prices, that can amplify those costs significantly during winter peak demand periods.

Businesses that treat natural gas as a simple commodity with a predictable cost trajectory are likely to be surprised by their 2026 bills. Those that incorporate forward market context into their procurement planning, whether through fixed-rate supply contracts, hedging strategies, or hybrid structures, are better positioned to manage that exposure before it becomes a budget problem.

Electricity Price Forecast for Businesses

There is no single US electricity price forecast that applies uniformly to every commercial energy buyer. The rate your business pays for electricity in 2026 is the product of several variables that interact differently depending on where you operate, how you consume energy, and when and how you procure supply. Understanding how each of these variables affects your cost outcome is more actionable than any single forecast number.

Market and Utility Territory

The most significant variable in any commercial electricity cost forecast is geography. Businesses operating in deregulated electricity markets, including most of PJM, ERCOT, NYISO, ISO-NE, and parts of the Midwest, have the ability to choose their retail energy supplier and select a contract structure that reflects their risk tolerance and market view. That optionality is a meaningful cost management tool that regulated-market customers do not have.

Within deregulated markets, utility territory matters because capacity and transmission costs vary by delivery point. A business in western Pennsylvania does not pay the same capacity tag as a business in northern New Jersey, even if both are in the PJM footprint and procuring supply from the same retail energy supplier. Locational cost differences are real, and they are not always reflected in the headline rate a supplier quotes without a detailed billing analysis.

Regulated-market customers have limited ability to act on forecast data. Their electricity rate is set by the state public utilities commission through a rate case process, and the primary levers available to them are demand management and energy efficiency rather than supply procurement strategy.

Contract Type

For deregulated-market customers, contract structure is one of the most consequential decisions in the procurement process.

Fixed-rate contracts lock in a supply price for the full contract term, insulating the customer from market movements in either direction for the duration of the agreement. In the current environment, fixed rates provide protection from further capacity cost increases and natural gas price volatility. The tradeoff is that a customer locked into a fixed rate cannot capture savings if market prices decline during the term.

Index and variable rate contracts float with wholesale market pricing, exposing customers to every upward movement in electricity and natural gas markets, including the demand and capacity pressures described above. For most commercial customers without the financial structure to absorb month-to-month cost variability, index exposure in the current market environment introduces more risk than the potential savings justify.

Hybrid block-and-index structures fix a portion of the customer’s load while leaving the remainder indexed to the market. For customers with significant off-peak consumption or operational flexibility to shift load during high-cost hours, this structure balances cost certainty on the base load with the ability to capture favorable pricing on the variable portion.

Load Profile and Timing

Two customers in the same utility territory procuring from the same supplier can pay materially different effective rates depending on their load profile and when they enter the market.

A business with a flat, predictable consumption profile and a low peak-to-average ratio carries a lower capacity tag than a facility with sharp demand spikes during summer peak hours. That difference flows directly into the supply rate. Customers who have invested in demand management, peak shaving, or building automation have a structural cost advantage over those who have not, and that advantage compounds across every contract renewal.

Timing matters because energy markets move. A buyer who engages the market 90 days before contract expiration, solicits competing supplier bids, and executes when the forward curve is favorable will consistently outperform a buyer who renews at the last minute with a single supplier offer. In a market where capacity costs are structurally elevated and natural gas prices are volatile, the difference between a well-timed and a reactive procurement decision can represent tens of thousands of dollars over a multi-year contract term.

The bottom line for commercial buyers: the 2026 electricity price forecast is directionally unfavorable relative to where rates were three to four years ago. But pricing outcomes are shaped by the decisions your business makes about market access, contract structure, and procurement timing. Buyers who approach those decisions deliberately are not at the mercy of the forecast. They are managing their exposure to it.

Natural Gas Outlook for Businesses

For commercial and industrial customers who purchase natural gas directly for heating, manufacturing, or process applications, the 2026 outlook calls for higher costs relative to the 2023 and 2024 lows and meaningful volatility around that elevated baseline.

Henry Hub forward prices for 2026 are trading in the $3.50 to $4.50 per MMBtu range depending on the delivery period, compared to the 2024 annual average of approximately $2.22 per MMBtu. That directional increase of 55 to 100%, depending on the month, reflects two structural changes in the domestic natural gas market that are not temporary. LNG export capacity has expanded to the point where international demand now competes directly with domestic consumption for available supply, raising the effective price floor for US gas buyers. Storage inventories have trended below seasonal averages, reducing the buffer that historically kept prices stable during demand spikes or production disruptions.

For businesses in the Northeast, the headline Henry Hub number understates actual procurement costs. Basis differentials, the spread between the Henry Hub benchmark and regional pipeline delivery prices can widen significantly during winter peak periods when pipeline capacity is constrained, and heating demand competes with gas-fired power generation for the same infrastructure. Northeast commercial customers who budget on Henry Hub alone without accounting for basis risk have consistently found their actual gas bills higher than projected during cold weather events.

The practical guidance for natural gas buyers in 2026 mirrors the electricity procurement advice above: fixed-rate supply contracts provide budget certainty in a market where the directional bias is higher and the downside risk of index exposure is meaningful. Customers currently on index or market-based gas supply should evaluate whether their financial structure genuinely supports that exposure or whether a fixed or hybrid structure better fits their operational reality.

Natural gas procurement timing follows similar seasonal logic to electricity. Spring and early fall tend to offer more favorable forward pricing windows than winter, when supply risk is being actively priced into near-term contracts. Working with a licensed energy advisor who monitors storage data, LNG export volumes, and forward curve movements on an ongoing basis ensures that procurement decisions are made when market conditions are favorable rather than when a contract deadline forces the issue.

What This Forecast Means for Commercial Energy Buyers

Market data and forecast summaries are only useful if they inform an actionable decision. Here is what the 2026 energy price outlook means in practical terms for the business decisions that matter most.

Budgets Built on Recent History Are Likely Understated

The 2022 through 2024 period saw meaningful energy cost volatility, but it also included periods of relative price relief, particularly in natural gas, where Henry Hub prices fell sharply from their 2022 highs and stayed low through much of 2024. Finance teams that anchored their 2026 energy budget to 2024 actuals or recent contract rates that predate the latest capacity auction results may be working with a cost assumption that does not reflect where the market is today. The 2026 forecast does not support the expectation that electricity or natural gas costs will return to 2023 or 2024 lows in the near term. Budget planning should reflect current forward market levels, not recent history.

Contract Renewals Require More Attention Than They Did Three Years Ago

In a stable or declining market, a renewal that happens on autopilot carries limited financial risk. In the current environment, that approach is significantly more costly. The gap between a competitively sourced renewal rate and a single-supplier offer has widened as capacity costs have increased and supplier margins have expanded in a market with less pricing pressure from buyers who do not shop. Businesses whose contracts expire in 2026 are renewing into one of the more consequential procurement moments in recent years. Treating that renewal as a transaction rather than a strategic decision is an avoidable mistake.

Procurement Planning Cannot Start at the Expiration Date

The 60 to 120-day window before contract expiration is the minimum lead time for a well-executed renewal. In a market with elevated forward prices and limited near-term relief on the horizon, starting earlier is prudent. Customers who engage the market 90 to 180 days before expiration have time to solicit multiple supplier bids, evaluate contract structures, monitor the forward curve for favorable entry points, and execute without deadline pressure. Customers who start at 30 days must accept whatever the market is offering at that moment, with whatever leverage remains when a supplier knows the customer has no time to walk away.

Exposure Management Is Not Just About Finding a Lower Rate

The 2026 forecast environment rewards businesses that think about energy cost management beyond the supply rate. Capacity tag reduction through peak demand management, demand response program enrollment, and building automation investments all reduce the cost basis that flows into the next supply contract. A business that lowers its measured peak demand before renewing a supply contract enters that negotiation with a structurally lower cost profile. Similarly, understanding whether your current contract type is actually aligned with your organization’s risk tolerance and financial structure is a more valuable exercise in the current environment than it was when energy prices were lower and more predictable.

The Forecast Is a Planning Input, Not a Prediction

No energy price forecast is a guarantee of where markets will be in six or twelve months. Forward curves can shift, storage conditions can change, and demand events can accelerate the trends described in this article. What the 2026 forecast provides is a directional basis for planning active procurement management rather than passive renewal. Businesses that treat this forecast as a planning input and act on it deliberately will be better positioned than those that wait for a clearer signal that may not arrive before their current contract expires.

What Businesses Should Do Now

Acting on the 2026 energy price forecast before your next contract renewal is what actually protects your budget. Here is a concrete action plan for commercial and industrial energy buyers who want to approach 2026 procurement deliberately rather than reactively.

Review Usage and Billing Data Before Renewal

Before you engage a single supplier or broker, pull at least 12 months of electricity and natural gas billing data across every meter and service account your business operates. This is the foundation of every procurement decision that follows.

Monthly billing data reveals seasonal consumption patterns, peak demand trends, and cost component breakdowns that are invisible without it. Where interval data is available through your utility’s online portal or smart meter program, download it at the 15 or 30-minute level. Interval data shows exactly when your facility is drawing its highest loads. This data is directly relevant to your capacity tag, your demand charges, and your ability to benefit from a block-and-index structure versus a straight fixed rate.

Businesses that enter a renewal conversation without this data are negotiating blind. They cannot evaluate whether a supplier’s offer reflects their actual load profile, cannot identify whether demand management investments would lower their cost basis before locking in a new rate, and cannot make an informed decision between contract structures. Twelve months of billing data takes an hour to collect and can meaningfully change the outcome of a procurement decision that will affect costs for the next one to three years.

Shop Before the Contract Deadline

The single most common and most costly procurement mistake commercial energy buyers make is starting the renewal process too late. Last-minute renewals eliminate leverage entirely.

A supplier negotiating with a customer who has 30 days until contract expiration knows that customer has no practical ability to walk away. The competitive pressure that drives suppliers to sharpen pricing disappears when timeline pressure replaces it. The result is a renewal rate that reflects the supplier’s margin objective rather than what the market would produce under competitive conditions.

The optimal window for beginning the renewal process is 90 to 120 days before your current contract expires. This lead time gives you the ability to solicit competing bids from multiple suppliers, evaluate offers across rate, term, and contract structure, monitor the forward curve for a favorable execution window, and still have time to walk away from an offer that does not meet your objectives. It also accounts for utility enrollment processing times, which can run four to eight weeks in some markets

If you are not certain when your current contract expires, find out today. That date is the most important number in your energy procurement calendar, and not knowing it is how businesses end up on post-term variable rates that erase the savings their prior fixed contract delivered.

Compare Fixed, Index, and Hybrid Structures

The 2026 market environment has made contract structure selection more consequential than it has been in years. The right structure for your business depends on the foundational question of your organization’s genuine tolerance for energy cost variability.

Fixed-rate contracts lock in a supply price for the full contract term. In the current market, a fixed rate could provide protection from further capacity cost increases, natural gas price volatility, and the demand-driven price pressure described throughout this article. For organizations where an unexpected 20 to 30% increase in energy costs would create a material financial problem, a fixed rate is the appropriate default in 2026 regardless of where the market is heading. Beware that many fixed-rate contracts allow suppliers to pass through cost adjustments related to future capacity auctions. It is prudent to read the details of your energy contract prior to signing.

Index and variable rate contracts float with wholesale market pricing, which means customers retain full exposure to every upward driver in the 2026 forecast. Index pricing makes sense for organizations with the financial structure to absorb monthly cost variability and the operational profile that allows them to benefit from favorable market hours. For most small to mid-sized commercial customers, index exposure in the current environment introduces more risk than the potential savings justify.

Hybrid block-and-index structures fix a defined portion of the customer’s base load while leaving the variable remainder indexed to the market. This structure is particularly well-suited to larger commercial and industrial customers with predictable base load and significant off-peak consumption. It delivers cost certainty on the core load while retaining the ability to capture favorable off-peak pricing on the variable portion. For customers who find the full fixed vs. full index decision too binary for their actual usage profile, a hybrid structure is worth evaluating seriously before the next renewal.

Use Market Guidance to Support Budgeting

Energy forecasts are most valuable when they are treated as planning inputs rather than news items to be read and set aside. The 2026 market data summarized in this article gives your finance team a directional basis for building energy cost scenarios into annual and multi-year budget models.

In practical terms, this means building at least two energy cost scenarios into your budget. One based on current forward market pricing for a fixed-rate procurement, and one that reflects the cost range of index or variable rate exposure, given the risk drivers described above. The spread between those two scenarios is the total dollar value of the risk you are either managing through fixed-rate procurement or accepting through index exposure.

For multi-site operators and larger commercial customers, this scenario planning exercise also reveals where energy cost risk is most concentrated across the portfolio, which locations are approaching renewal in the highest-risk market windows, and where demand management investments would reduce the cost basis before the next procurement cycle.

A qualified energy advisor can provide market-specific forward pricing data, capacity cost projections, and contract structure modeling to support this budgeting process directly. The forecast tells you where the market is. The advisor translates that into what it means for your specific accounts, your renewal timeline, and the procurement decisions in front of you.

How Diversegy Helps Businesses Navigate Energy Price Volatility

Diversegy is a full-service commercial energy brokerage and a wholly-owned subsidiary of Genie Energy (NYSE: GNE), with access to 60-plus retail energy suppliers across all deregulated US markets and the market expertise to translate forward price data into procurement decisions that protect your budget.

Our team monitors electricity and natural gas forward curves, capacity auction results, and storage data on an ongoing basis, so when market conditions create a procurement opportunity, our clients are positioned to act before that window closes. When it is time to renew, we go to market on your behalf, solicit competing supplier bids, evaluate each offer across rate, contract structure, and term, and present a clear comparison that gives you the context to make a deliberate decision rather than a reactive one.

For multi-site portfolios, we manage the entire procurement process centrally, aligning contract terms, tracking expiration dates, and ensuring no account rolls onto a post-term variable rate through inaction or missed deadlines. If your energy contract is approaching expiration or you are unsure whether your current rate structure is aligned with the 2026 market environment, contact our team of energy market experts for a complimentary review and supplier comparison.