As of 2026, energy markets are operating under conditions that make the index vs. fixed decision genuinely complex. Natural gas storage levels have trended around the five-year seasonal average, keeping forward prices elevated. Electricity forward markets remain elevated across major grid regions, driven by record PJM capacity auction results, tightening reserve margins, and accelerating load growth from data centers. In this market, index pricing requires a clear-eyed view of your organization’s financial tolerance and market outlook before committing.

This article explains how energy index pricing works, which businesses are best suited for index or hybrid rate structures, and how to evaluate whether floating the market makes sense for your organization, given current forward market conditions.

What Are Energy Index Rates?

In today’s market, where electricity forward prices remain elevated, and demand for natural gas continues to create volatility, understanding exactly what you are signing up for when you choose an index rate has never been more important.

Unlike fixed-rate prices that do not change for a pre-defined period of time, energy index rates float up and down with the electricity and/or natural gas markets. There are different types of hybrid retail energy contracts that include index rates as part of their terms and conditions. Let’s explore the various types of retail agreements available to commercial customers and how index pricing works.

Block + Index

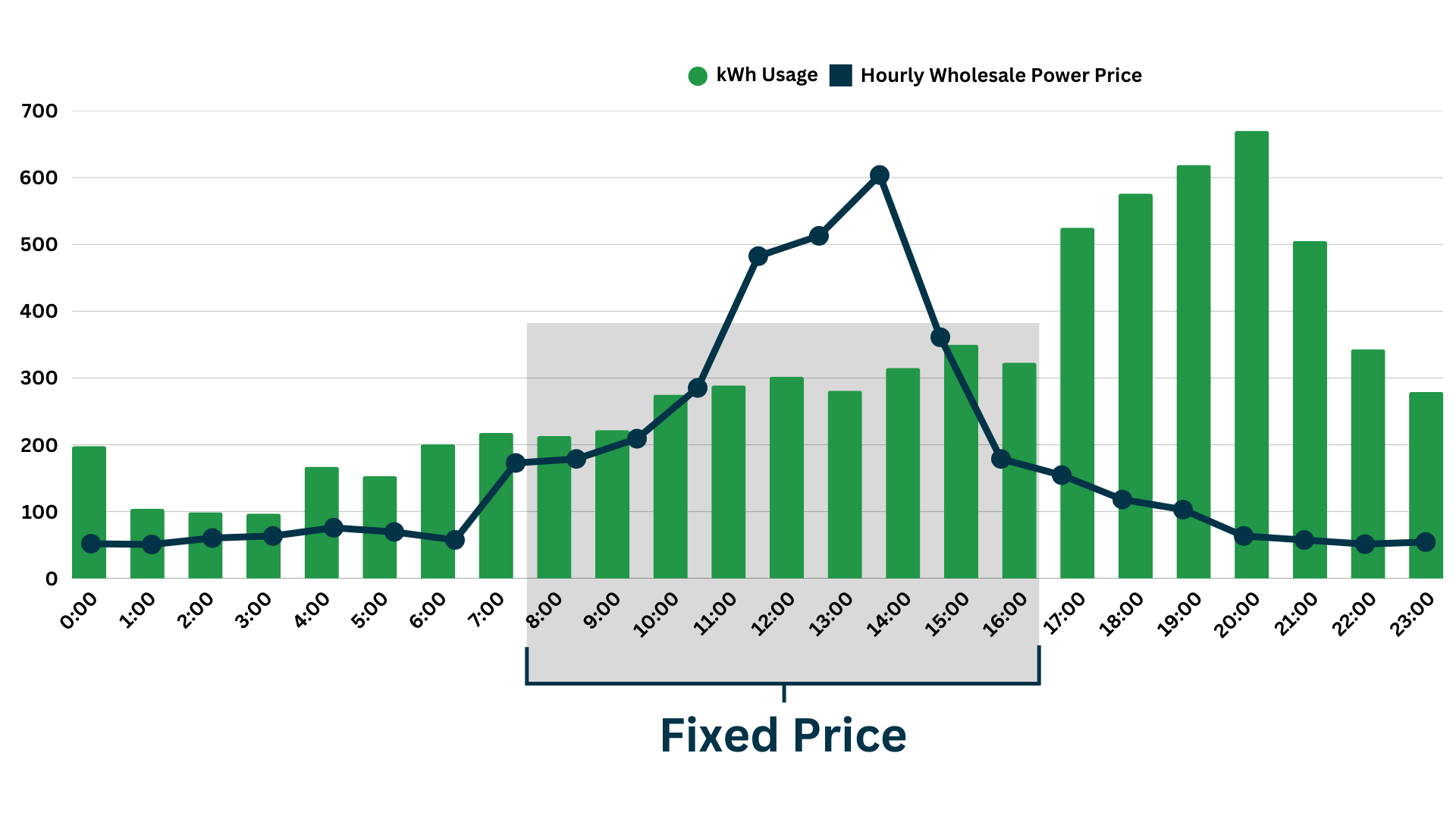

A block-and-index retail energy supply contract might be a good-fit when evaluating energy supply product options. This price structure allows a customer to lock in a defined percentage or volume of their total energy load at a fixed price, while floating the remaining portion on the index market. The result is a single supply agreement that carries both price certainty and market exposure.

The fixed block is typically sized to cover a customer’s base load, or on-peak load. The indexed portion covers the remainder, floating with wholesale market pricing and capturing savings when spot prices are favorable, particularly during off-peak periods when demand is lowest. Let’s illustrate how this works in practice:

- A manufacturer running third-shift with significant off-peak energy load, might block 400 kW of on-peak load

- The remaining load, concentrated in off-peak and overnight hours when wholesale prices are typically lower, floats on the index market, allowing the facility to capture favorable off-peak pricing on the variable portion of their consumption without exposing their entire load to market volatility.

The financial outcome of this structure is a blended effective rate that sits between the fixed block price and whatever the index delivers on the floating portion.

Who Block + Index Is Best For

Block-and-index products are particularly well-suited for large commercial and industrial customers with mixed load profiles, or operations where a meaningful portion of consumption occurs during off-peak or overnight hours when index pricing consistently trades below on-peak levels. Facilities that benefit most include:

- Large manufacturers with continuous or near-continuous production schedules that include significant overnight and weekend operating hours

- Cold storage and refrigerated warehouse facilities where compressor loads run around the clock but can be partially shifted to off-peak windows

- Data centers and technology facilities with predictable base load and variable peak demand tied to traffic patterns

- Food and beverage processors with flexible scheduling that allows energy-intensive processes to be shifted toward lower-cost index hours

- 24/7 water or sewer plants where off-peak energy consumption is significant and load is consistent throughout the remaining hours of the day.

For customers without significant off-peak consumption or with highly variable and unpredictable load profiles, a block-and-index structure may not deliver the same value. The indexed portion needs to represent load that realistically benefits from off-peak market pricing to justify the added market risk.

Fixed-Adder

A fixed-adder product allows a customer to purchase energy at wholesale market prices plus a fixed supplier margin, making it a fully variable rate structure where the total cost moves up and down with the market in real time. Unlike a fixed-rate contract where the supplier assumes the price risk for the duration of the term, a fixed-adder passes market exposure directly to the customer while the supplier earns a predetermined, transparent margin on every unit delivered.

How Fixed-Adder Pricing Works

The mechanics of a fixed-adder product differ slightly depending on the commodity:

- For Electricity: Fixed-adder pricing is typically calculated as LMP (wholesale price at the customer’s location) plus the supplier’s fixed margin expressed in cents per kilowatt-hour. The LMP component reflects real-time or day-ahead wholesale index market conditions at the specific node on the grid where the customer takes delivery. These prices can vary by location based on transmission congestion and local grid conditions. A customer on an LMP+ structure paying a $0.008/kWh fixed adder during a period when the day-ahead LMP averages $0.055/kWh would pay an effective rate of $0.063/kWh for that billing period. That same rate shifts each month as the LMP moves.

- For Natural Gas: Fixed-adder pricing is commonly structured as NYMEX (New York Mercantile Exchange Henry Hub futures price for the delivery month) plus the supplier’s fixed margin expressed in cents per therm or dollars per MMBtu. Customers procuring natural gas on a NYMEX+ basis should also be aware of basis differentials, or the spread between the Henry Hub benchmark price and the actual price at the local delivery point where gas is physically delivered. Basis differentials vary by region and pipeline, and they can widen significantly during periods of regional demand or pipeline capacity constraints. Notably, in the Northeast during winter peak periods, local basis has historically spiked well above Henry Hub during cold weather events. A customer assuming their NYMEX+ rate reflects their all-in gas cost without accounting for basis is exposed to a cost component that can move significantly and independently of the NYMEX benchmark index.

Who Fixed-Adder Products Are Best For

Fixed-adder products are most appropriate for businesses that treat energy as a cost of goods sold and have the financial structure to absorb market price variability. For example, a petroleum refinery using electricity to process crude oil may elect a straight LMP+ structure because the cost of electricity is embedded in the price of the refined product and can be passed through to end customers. Similarly, a liquefied natural gas facility purchasing gas on a NYMEX+ basis is often naturally hedged against price movements because its revenue is also indexed to market gas prices.

Fixed-adder products require active market awareness and a genuine tolerance for cost variability. For businesses where an unexpected energy cost increase cannot be absorbed or passed through, the fully variable nature of a fixed-adder structure introduces more risk than the potential market savings justify.

Straight Index

A straight index electricity product is another market-exposed rate structure available to commercial energy customers. Unlike a fixed-adder that prices against a monthly average wholesale benchmark, a straight index product calculates the customer’s energy cost on an hourly basis in real time, multiplying the actual index rate for each hour by the total kilowatts consumed during that hour, plus a fixed markup for the energy supplier.

During periods of low demand and favorable market conditions, straight index customers can capture extremely competitive pricing that no fixed-rate contract can match. During periods of high demand, straight index customers absorb the full cost of those market spikes in real time, with no protection and no recourse until the hour passes.

These products are calculated as follows:

(Hourly LMP + Fixed Markup) x (Customer Hourly Load)

For organizations where energy is a fixed operating cost rather than a pass-through item, straight index is rarely the appropriate procurement choice. The potential for savings during favorable market periods exists, but the downside exposure during adverse conditions is uncapped and can produce cost outcomes that are materially damaging to budgets.

Benefits Of Index Pricing

There are many reasons why a business or organization might choose to enroll in an index-based energy plan or some sort of hybrid rate.

Off-Peak Usage: If you are using lots of energy during off-peak hours, then you might be able to save money by enrolling in an index rate during those times. Energy prices are typically lower during off-peak periods when consumer demand is low.

Cost Of Goods: When your utility expenses are directly related to your cost of goods, or your cost to produce a product, then an index rate tied to the market could be a good option for you. If your industry typically passes down the cost of energy to your customers, then a volatile energy market does not have an effect on your bottom line.

Flexibility: Index-based contracts also offer flexibility to energy users. Signing up for a fixed rate bounds you to the terms of your contract, while an index product allows you to float the market and potentially lock-in when prices are more favorable.

Risks of Index Pricing

Index and variable rate products offer genuine advantages for the right customer, but those advantages come with a risk profile that deserves explicit attention. The risks of index pricing have materialized repeatedly in real markets, with real financial consequences for customers who were not fully prepared for what uncapped market exposure can mean.

Price Spikes During Extreme Weather Events

The most acute risk of index pricing is exposure to wholesale price spikes driven by extreme weather events, such as Winter Storm Uri (February 2021). This event remains the most vivid recent illustration of this risk. When a historic cold snap swept across the central United States, natural gas supply froze at the wellhead, gas-fired generation went offline across Texas, and wholesale electricity prices in the ERCOT market spiked to the market cap of $9,000 per megawatt-hour, and sustained for days. Commercial and industrial customers on straight index or variable rate products in these markets received electricity bills that were, in some cases, ten to twenty times higher than their normal monthly cost. Businesses that had operated on index products for years without incident absorbed losses in a single billing period that erased years of accumulated savings.

Budget Unpredictability

Beyond weather-driven spikes, the reality of index pricing is that energy costs become genuinely difficult to forecast and budget around on a consistent basis. Monthly energy bills on an index product can vary by 20, 30, or 50 percent or more from one billing cycle to the next.

For organizations that manage annual operating budgets, present energy costs to boards or investors, or operate in industries where margin predictability matters, this variability introduces a planning problem. A budget built on last year’s average index cost may be materially wrong by mid-year if market conditions change. An index customer has no reliable basis for projecting what next month’s bill will look like, let alone next quarter’s.

This unpredictability is manageable for organizations with strong cash flow and the operational discipline to monitor market conditions continuously. For businesses that do not meet the criteria, index pricing introduces budget risk that is difficult to hedge after the fact.

Fixed vs. Index vs. Block + Index: Rate Structure Comparison

Selecting the right energy rate structure is one of the most consequential procurement decisions a commercial energy buyer makes. The table below provides a direct comparison across the factors that matter most.

| Fixed Rate | Straight Index | Fixed-Adder (Index + Margin) | Block + Index | |

| Pricing Mechanism | Set price per unit for full contract term | Real-time hourly LMP × actual consumption | Wholesale benchmark (LMP or NYMEX) + fixed supplier margin | Fixed price on blocked volume; index rate on remaining load |

| Price Certainty | Full – rate locked for contract term | None – changes every hour | None on energy; margin component is fixed | Partial – fixed on block, variable on indexed portion |

| Budget Predictability | High – costs fully forecastable | Very low – hourly market exposure | Low – monthly average market exposure | Moderate – base load predictable, variable portion fluctuates |

| Market Upside Potential | None – locked in regardless of market movement | Full – captures every market low in real time | Full on energy component | Partial – indexed portion captures market improvement |

| Downside Protection | Full – insulated from spikes for contract term | None – fully exposed to price spikes | None on energy component | Partial – fixed block insulates core load |

| Capacity Cost Protection | Typically yes – embedded at execution | No – pass-throughs apply as incurred | No – pass-throughs apply as incurred | Partial – fixed block protected, indexed portion exposed |

| Weather Spike Risk | None during contract term | High – fully exposed (e.g. Winter Storm Uri) | High – monthly average absorbs spike periods | Moderate – fixed block limits exposure |

| Basis Differential Risk (Gas) | None – embedded in fixed rate | Applies – local delivery spread above Henry Hub | Applies – NYMEX+ does not include basis | Partial – applies to indexed gas portion only |

| Active Management Required | Low – rate set at execution | Very high – continuous market monitoring | High – market awareness and bill review | Moderate – indexed portion benefits from oversight |

| Contract Term | 6–60 months | Month-to-month or short-term | Month-to-month or short-term | Typically 12–36 months |

| Early Termination Risk | High – ETFs apply if exited early | Low – short commitments lapse naturally | Low – short commitments lapse naturally | Moderate – depends on fixed block term |

| Energy Treated As | Fixed operating expense | Cost of goods sold or pass-through item | Cost of goods sold or pass-through item | Either – depends on load split |

How Index Pricing Is Calculated

There are different ways to calculate energy index rates based on the commodity, energy contract type, and energy supplier. Natural gas index rates are calculated using futures contract settlement prices, while electricity index rates are calculated using real-time or day-ahead wholesale market pricing. Let’s explore both commodities below:

Natural Gas

The price of a natural gas futures contract moves up and down with supply and demand dynamics in the natural gas market. Each monthly futures contract has a specific expiration date. Here is how current natural gas futures contracts are structured:

- The February 2026 contract expires on 1/29/2026

- The March 2026 contract expires on 2/26/2026

- The April 2026 contract expires on 3/27/2026

These expiration dates represent the last trading day for each month’s futures contract. When a retail energy supplier is purchasing natural gas on the index market to supply a commercial customer, the price for a given month is typically determined by the settlement price of the corresponding futures contract on its expiration date. Here is how that calculation works in practice:

- A supplier is selling a natural gas index rate to a commercial customer

- The agreed pricing formula between the supplier and customer is: (NYMEX Henry Hub settlement price on last trading day) + ($0.50/DTh fixed supplier adder)

- The March 2026 contract settles at $3.85/DTh on its expiration date of 2/26/2026

- The total index price for the customer’s March 2026 supply is $4.35/DTh ($3.85 + $0.50)

This calculation repeats each month as the next futures contract expires, meaning the customer’s effective natural gas rate changes monthly in step with wherever the NYMEX Henry Hub market settles. As noted earlier, customers procuring natural gas on a NYMEX+ basis should also be aware that local basis differentials (the spread between Henry Hub and the actual regional delivery point) are not captured in this calculation and can add meaningful cost depending on the customer’s location and the time of year.

Electricity

Electricity index pricing works differently from natural gas because electricity cannot be stored at scale. It must be generated and consumed in real time. Rather than settling monthly against a futures contract, electricity index rates are calculated on an hourly basis using wholesale market prices that reflect actual grid conditions as they occur.

Electricity prices in the wholesale market are published hourly by the ISO or RTO responsible for managing the grid in a given region. These published settlement prices, known as Locational Marginal Prices (LMPs), reflect the cost of supplying the next unit of electricity at a specific delivery point on the grid, accounting for generation costs, transmission congestion, and line losses. When a commercial customer signs an index electricity supply agreement, their bill is calculated by multiplying the ISO-published LMP for each hour by the actual kilowatts consumed during that hour, plus the supplier’s fixed adder.

Here is an example of how electricity index prices are calculated using a realistic 2025/2026 PJM pricing scenario:

- Supplier agrees to sell customer electricity using the following formula: (hourly PJM LMP + $5.00/MWh fixed supplier adder)

| Hour | PJM Day-Ahead LMP ($/MWh) |

Supplier Adder ($/MWh) |

Total Rate ($/MWh) |

Customer Usage (kWh) |

Hourly Cost |

| 12:00 AM | $28.14 | $5.00 | $33.14 | 180 | $5.97 |

| 6:00 AM | $34.22 | $5.00 | $39.22 | 220 | $8.63 |

| 9:00 AM | $52.80 | $5.00 | $57.80 | 410 | $23.70 |

| 12:00 PM | $67.45 | $5.00 | $72.45 | 480 | $34.78 |

| 3:00 PM | $89.30 | $5.00 | $94.30 | 510 | $48.09 |

| 6:00 PM | $74.60 | $5.00 | $79.60 | 460 | $36.62 |

| 9:00 PM | $41.75 | $5.00 | $46.75 | 290 | $13.56 |

| 11:00 PM | $26.90 | $5.00 | $31.90 | 160 | $5.10 |

The table illustrates a critical characteristic of straight index electricity pricing. Costs are not evenly distributed across the day. For a customer consuming 510 kWh at 3:00 PM, the hourly cost is more than eight times what they pay for 160 kWh at 11:00 PM, driven almost entirely by the difference in wholesale LMP rather than consumption volume.

The ISO-published LMP settlement prices referenced in these calculations are publicly available through each regional operator’s market data portal. PJM publishes day-ahead and real-time LMPs at the nodal and zonal level through its Data Miner platform; ERCOT publishes Settlement Point Prices through its market information portal; NYISO and ISO-NE publish comparable hourly settlement data through their respective market portals. Retail energy suppliers use these published prices as the basis for index billing.

When Should Your Business Consider Index Pricing?

Index pricing is not appropriate for every commercial energy customer, but for the right organization, it can deliver meaningful cost advantages over a fixed-rate alternative. The four questions below provide a practical decision framework for evaluating whether index pricing makes sense for your business.

1. Can Your Business Absorb Monthly Price Swings of 20–40%?

This is the foundational question, and it deserves an honest answer before any other factor is considered. Index electricity and natural gas costs can fluctuate by 20 to 40 percent or more from one billing period to the next. During extreme market events, the variance can be significantly larger.

If a 20 to 40 percent increase in your monthly energy bill would create a material budget problem, your business does not have the financial structure to manage index exposure responsibly. A fixed or hybrid rate structure is the more appropriate foundation. If your organization has the financial flexibility to absorb that variability without operational consequence, index pricing becomes a viable option worth evaluating further.

2. Do You Have Significant Off-Peak Usage?

The economic case for index pricing strengthens considerably when a meaningful portion of a customer’s energy consumption occurs during off-peak hours, when wholesale LMPs are consistently lower than on-peak rates.

A facility that operates primarily during daytime on-peak hours faces the full volatility of index price without the offsetting benefit of capturing low overnight pricing. A facility with significant off-peak load has a consumption profile that is structurally positioned to benefit from hourly index pricing.

Before committing to an index product, analyze your interval usage data to understand what percentage of your consumption falls into off-peak versus on-peak windows. If the majority of your load is concentrated in on-peak hours with limited off-peak consumption, the index pricing model works against your cost profile rather than in its favor.

3. Is Energy a Pass-Through Cost in Your Product Pricing?

The business types best suited to index pricing share a common financial characteristic. Energy is a cost of goods sold that is embedded in the price of their product or service, rather than a fixed operating expense that must be absorbed within a set budget. When energy costs rise, product pricing adjusts. And when energy costs fall, margins improve. This pass-through dynamic neutralizes the downside of index exposure by linking energy cost variability to revenue variability, rather than a fixed budget item.

Oil refineries, petrochemical processors, LNG facilities, manufacturers with indexed product pricing, and certain wholesale commercial operations all share this characteristic to varying degrees. For these organizations, index pricing is structurally rational because their revenue model is already structured to energy market movements.

4. Are Current Forward Curves in Contango or Backwardation?

Even for businesses that meet the first three criteria, market timing matters. The shape of the forward curve at the time you are evaluating an index product provides important context for whether floating the market makes sense right now.

Backwardation, when near-term prices are higher than forward prices, suggests the market expects prices to decline over time. In a backwardated environment, index customers who can absorb near-term volatility may benefit as prices ease lower over the contract horizon. Fixed-rate customers locking in during backwardation are capturing rates that reflect today’s elevated near-term market, while index customers retain the ability to benefit from the expected price decline.

Contango, when forward prices are higher than near-term prices, signals that the market expects prices to rise. Entering an index product in a contango market means the customer is accepting near-term pricing that is currently favorable relative to the forward curve, but retaining full exposure to the market as prices move higher. For customers with low risk tolerance, a contango curve is a signal to consider locking in a fixed rate before that forward premium materializes in spot pricing.

As of early 2026, electricity forward markets in key regions, including PJM, remain elevated relative to historical norms, driven by capacity auction results, load growth from data centers, and tightening reserve margins. Natural gas forward markets are reflecting below-average storage levels and sustained export demand. In this environment, businesses considering index pricing should do so with a clear understanding that the current forward curve is not offering a favorable entry point.

If your answers to these four questions suggest that index pricing could be appropriate for your business, the next step is a detailed load profile analysis and a forward market review with a qualified energy advisor. Diversegy works with commercial and industrial customers across all major deregulated markets to evaluate rate structure options objectively. Contact our team to discuss your current energy cost structure and where the market stands today.

Want To Learn More About Index Rates?

In conclusion, index energy pricing can be a great tool for certain businesses based on their usage patterns. Index rates can be beneficial for businesses with off-peak usage, those that want more flexibility, or those that can pass through the cost of energy to their customers. If you are looking to learn more about energy markets, index products, or hybrid energy contract structures, contact our team of energy professionals today.